0 to 1 in Crypto: Grasping Blockchains, their Applications & future Impact

voynichsadventure.substack.com

0 to 1 in Crypto: Grasping Blockchains, their Applications & future Impact

Thesis on Blockchain Technology, its Applications and their impact on the Internet, Societies and Companies. Its History, its Current State and its Future.

This paper is meant to provide a high-level view on Blockchain technology and its impact on the internet, societies and companies. Borrowing from the Crypto world’s greatest minds, we aim to understand the evolution of communication systems, and how crypto networks such as Bitcoin and Ethereum fit in with their original trust networks. Additionally, we reflect on Crypto’s fundamental revolution of the internet, privacy, and real-world applications for developing and developed economies. Furthermore, we dive into the question of why now is the right time to focus on Crypto for builders and for investors before exploring how profound the impact of Crypto has been on traditional hierarchical structures within startups and investment firms. This paper is meant as a starting point, aiming to educate rather than confuse, hoping to spark the interest of many and providing guidance on a new industry domain. For the author the original motivation was to build a coherent first principles view on the space and challenge our conviction on Crypto - independent of price actions, “Fear-of-missing-out”, political pressure and reputation. We conclude that our conviction firmly holds.

1. The Traditional Database and the Need to Trust the Middleman

In arguably one of the most significant technological inventions of the past 50 years, Satoshi Nakamoto conceptualized the first decentralized Blockchain database with the invention of Bitcoin in 2008.

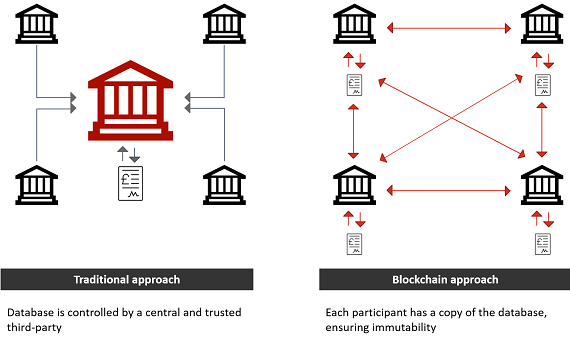

Originally, databases were records of information controlled by centralized single entities and stored on local computers or servers. Conceptually, imagine a database to be an Excel file stored on a single computer - the file owner can quickly and easily write, replace or delete all the input values. As databases were controlled by single entities, the users had to trust that these entities were correctly taking care of the data (= records of information). Concretely, users had to trust the centralized entities not to tamper with the records, delete information (i.e.: your address), steal information (i.e.: sharing the social security number with someone else) or change balances (i.e.: money balances).

Let’s go through a simplified example: Imagine Lisa owns $10 and this information is stored within the bank’s proprietary database. Suddenly, the bank manager does not like Lisa anymore and deletes the $10 from her account, or even worse transfers the money to his account. Concretely this means that the bank owner altered the database after the original entry has been created - thereby, ex-post changing the ownership over the $10. As the bank manager is the sole controller of the database, there is no common consensus who owns the $10 (= Lisa says it’s her money, the manager says it is his money). Extrapolating from this example, users (i.e.: Lisa) need to trust the owners of the database (i.e.: the bank manager) that they are doing the right thing. As the entries from the database are hidden, users are not able to verify the results themselves. As a result, they have to trust the owners of the database.

Due to its properties, the database owner can itself change the database without leaving any trace - meaning that the bank manager can transfer the $10 and delete all evidence that Lisa had $10 in the first place. Therefore, users are highly dependent on the goodwill of the database operator - as they control our data or in the case of banks, our money.

Enter Blockchains - Building a Trustless Database

As mentioned, imagine the traditional database being an Excel file stored on a single computer - the file owner can quickly and easily write, replace or delete all the input values. Using the same analogy, a Blockchain would be a globally-shared, append-only (= you cannot alter the original content) with advanced Macros (in the case of Ethereum).

Exhibit 1: The traditional Database can be altered at any time. In the Blockchain, the previous state (within the red box) cannot be altered. One is only able to add to the state and not change the state.

Simplified, after each state at time t, t+1, t+2,..., t+n, the blockchain takes a screenshot of the account balances of Lisa, Paul and Richard. This screenshot is then stored in a cardboard box (= the block), which we then close and seal. Every new state is added on top of the latest block - a chain is formed, giving the database the name Blockchain.

Let’s go through a simplified example. Lisa, Paul and Richard are having a poker night. Some win, some lose - the key is that the account balance changes. The next day (t+3), the friends sit together and agree (= find consensus) on the new money balances and write the balances into the blockchain - the new block at t+3 is added on the latest block t+2. If - a few days later - Paul is curious how much money they lost during the poker tournament, he is able to check his balance at state t+2 and his balance at t+3. As Lisa, Paul and Richard agreed on the new status at t+3 and all of them store one version of the database, Paul is not able to cheat. He would be able to change his balance at t+3 to $100, but Lisa and Richard know that Paul has tried to cheat as they have their own local copy of the Blockchain.

Exhibit 2: Less simplified, this is how a Blockchain looks like - a chain out of data blocks. A single block consists of a block header and a block body. The header contains data such as the hash of the previous block, a timestamp etc. The body contains all the transactions included in this block. Once a block has been created (information put inside a block) one cannot go back and change the information. It is forever stuck in the block. However, anyone is able to see the information.

This means, rather than trusting a centralized, hidden database which is controlled by one party, Blockchain technology allows everyone to have their own copy of the database, which consists of blocks of information. In short, after some time period a group of decentralized actors agrees on a consensus. This consensus is saved and everyone gets a copy of the latest consensus. Every second, minute or hour a new block emerges with the new state (= status of information) - making the blockchain longer and longer.

By agreeing on a global consensus, sharing the data across many participants, users no longer need to trust the data owners. Suddenly, users are able to verify information themselves on the blockchain. As blockchain data cannot lie, users are not required to trust anymore, making them trust-minimized databases.

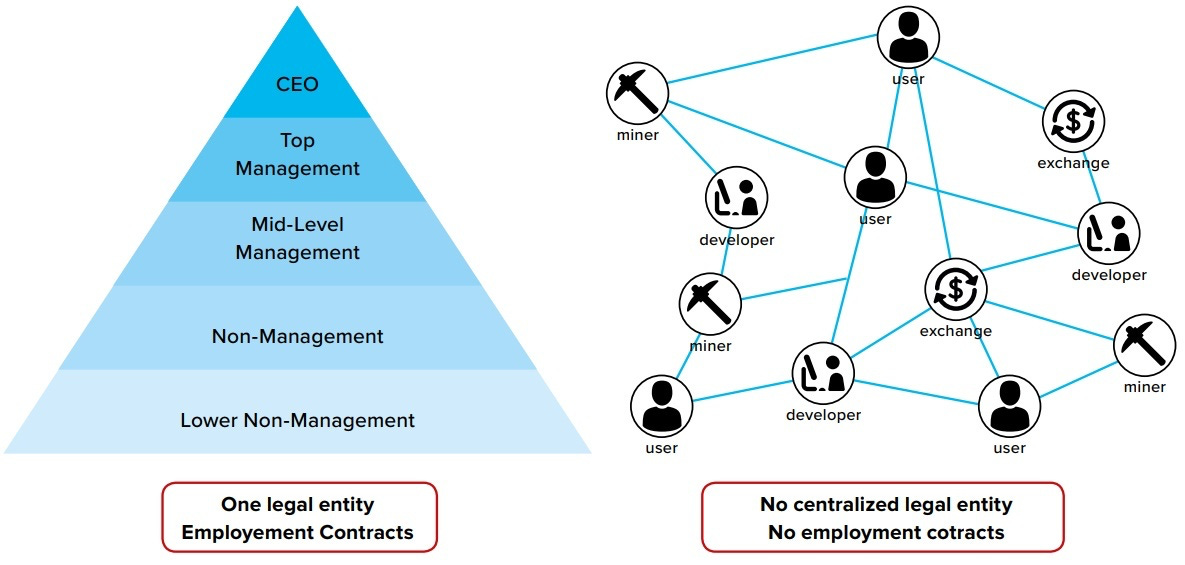

Exhibit 3: Centralized databases controlled by a single entity. Decentralized databases where every participant (node = computer) has a copy of the database.

Basically, Blockchain is just another (r)evolution of the traditional database. The core function of the original database was to allow users to store information. Over time, as more data was stored, more proprietary databases were created - suddenly every company had their own database. In order to transfer information between different entities, proprietary databases are communicating with each other - imagine a long supply chain of different databases transporting information. With the emergence of the blockchain database, we can merge all the proprietary databases into one, single database, practically taking out all the different database “middlemen”. As a result, the transfer of information between 2 parties became much more efficient.

Think of it with a simple example. Imagine 2 stock traders - one wants to buy, one wants to sell. In order to execute the trade, many different databases transfer information between each other (i.e.: Stock broker A → Bank A → Exchange → Bank B → Local Bank B → Stock broker B). With a blockchain, we eliminate many of those entities in the middle, storing the data in a public database. This makes the transfer of value and information significantly more efficient as the supply chain of different databases collapses. Taking out the middleman and building trust between different actors of the society is the achievement of blockchain technology.

Blockchain’s Key innovations

Through Bitcoin, the first decentralized blockchain database was conceptualized. However, what could be the impact of this database revolution? Just like the invention of the wheel had a revolutionary impact on human civilisation, and just like the invention of transistors led to the rise of computers, open decentralized databases (= Blockchains) are also expected to have a profound impact on the internet and human society. However, just as the impact of the invention of transistors took many years to lead to the wide-spread adoption of computers, it may take decades to explore the full impact of blockchains

Exhibit 4: As usual, it is hard to predict how technology will be used in the early days

For us, Blockchain’s innovations are three-fold from a first-principles basis:

Ownership rights on the internet: Through blockchains, users can bring ownership to the internet. In the real-world, humans have developed property rights, giving them ownership over land, house and business. Property rights are issued by the state and backed by strong laws. As a result, nobody can just come and take their property away. Due to property rights, owners have the right motivation to further develop their property and improve it for following generations.

However, in the stateless internet with thousands of different actors, there is no central authority and no consensus on who owns what. Through blockchain technology humans have been able to create an open, decentralized database which is not controlled by anyone. As we are able to agree on a common consensus, we are able to agree on who owns property on the internet. This means that for the first time in our history we are able to bring property rights and ownership on the internet. Rather than having the need to trust a bank or another centralized authority, an open decentralized database aka the blockchain shows who owns what.

For instance, in the offline world, when users deposit savings into their local bank, they receive an IOU, basically a promise from the bank that they can withdraw their money whenever they want. However, if the bank goes insolvent, user deposits (= their money) is used to cover the banks’ debt obligations - exactly what happened to Greek banks during the Euro-crisis. The only type of money that really belongs to the owners is the cash (“fiat = currency not backed by a commodity like USD, EUR, GBP”) they hold physically in their hands.

In the offline world, the fact that humans physically hold cash makes them the owner of the cash. In the online world, the blockchain holds the globally agreed consensus. As the blockchain attributes digital assets to the owner, the owner automatically receives ownership rights. Therefore, users can hold digital assets through self-custody. Rather than a local bank and their database telling users that the assets belong to them, the blockchain database with a global consensus tells users that the assets belong to them. Nobody can take ownership away as only the users themselves know the secret private key. Therefore, only the holders of the private key can access the money, conduct transactions or sign contracts. Not the bank manager, just the users themselves.

This is why Crypto advocates the value of self-custody of assets and data. For instance, the reason why people lost money with FTX was because users gave away their Crypto assets to a “bank” (= FTX), which handed them an IOU. Due to fraud, FTX lost the money, the IOU was worthless and users lost their savings.

Permissionless access to novel applications: Secondly, as the blockchain and its applications are of permissionless nature they are not controlled by a single entity or any single person. This means, anyone - regardless of religion, race, sex or gender - can build ownership, share information and interact with each other. Nobody can censor their transactions and their actions. In countries where repressive regimes are in place, individuals are finally able to build (digital) ownership, create wealth and share information thanks to a free and open internet. This is why Crypto advocates for decentralization (= not controlled by a single entity) and permissionless innovation (= everyone can join and build on top).

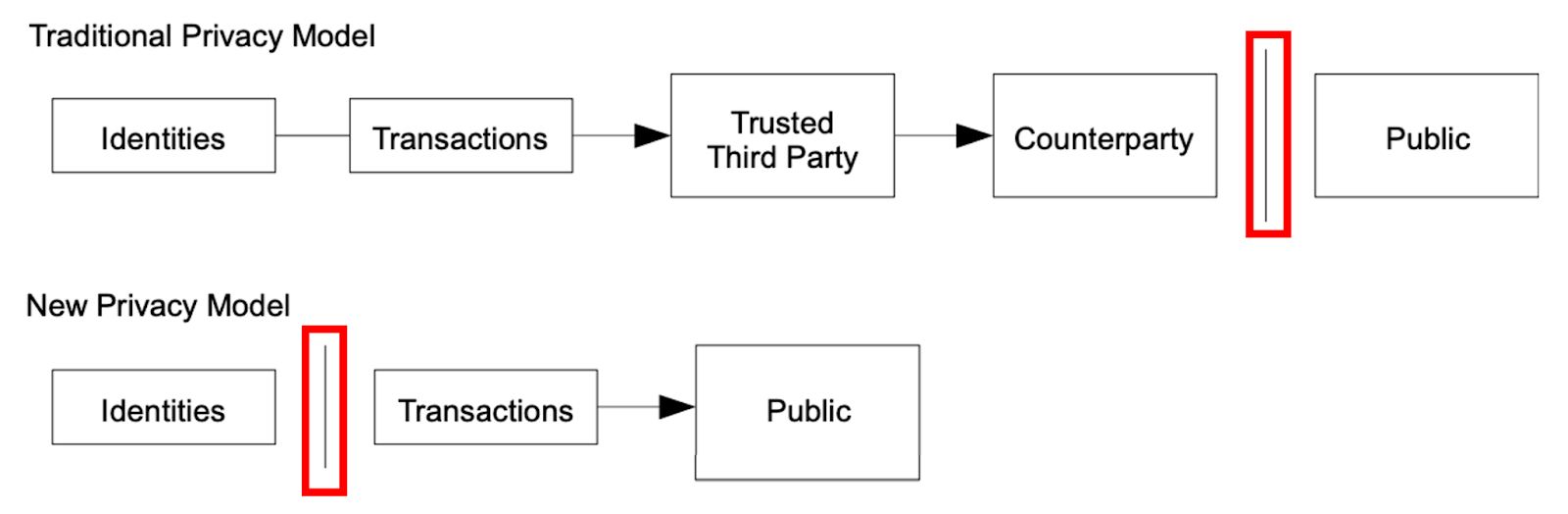

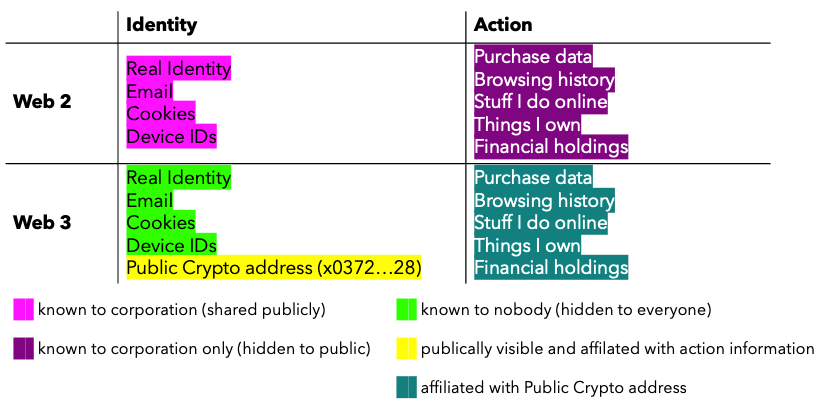

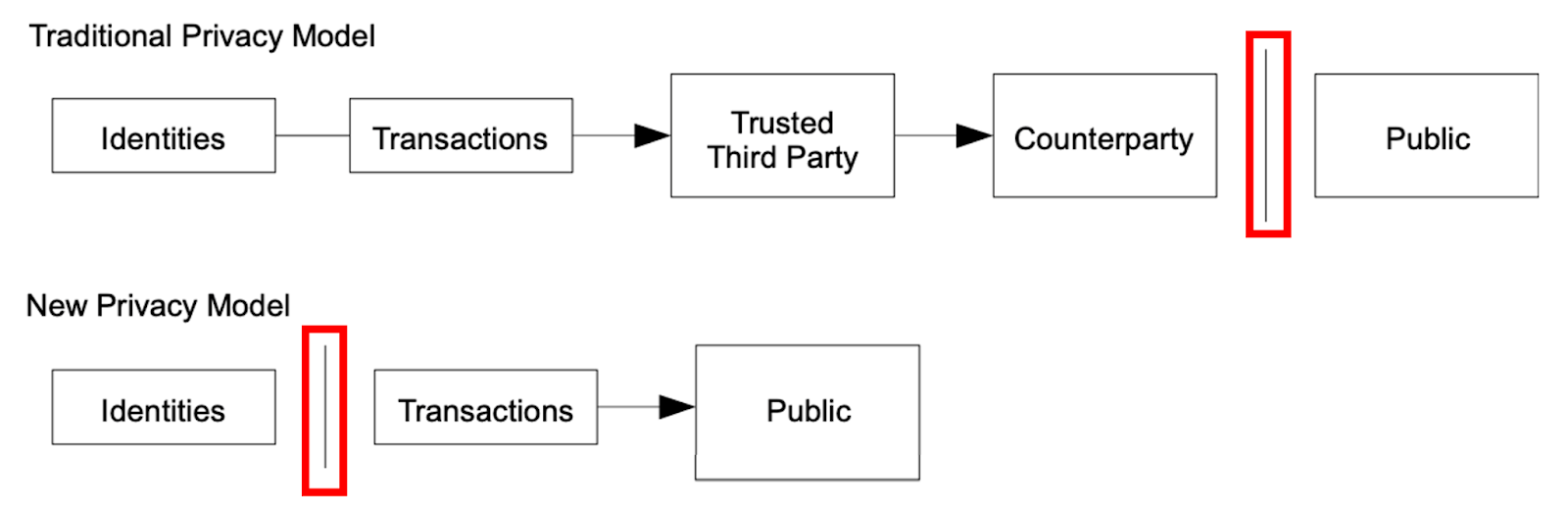

New Privacy Model: Thirdly, Blockchains have revolutionized privacy on the internet. In Web2 (= today’s internet relying on centralized databases), the user’s real identity, email and physical addresses are known by data owners (Google, Facebook, etc.). If requested, the data owners have to share user data with governments. For example, the requests for Google’s user data by the U.S. government has increased by 510% since 2010. Although concerning, this might not be a problem for users in Europe and the US. But what about users in China, Libya or Russia? In Web3/Crypto (= internet relying on decentralized databases) the real user identity is separated from the “public” address, which users are using to interact online. This allows users to become fully anonymous, which is of fundamental importance in countries with repressive governments. This is why Crypto advocates strong privacy, while maintaining complete transparency of what is happening.

Exhibit 5: Bitcoin’s whitepaper shows the separation between the real user identity and online transactions. In traditional privacy models the link between identity and (trans)actions is publicly known to data owners such as Google or Facebook. Within Crypto’s new privacy models, there is no link between (trans)actions and identities as transactions are only displayed with a digital address (x038137…23 sends $3). The real identity is hidden and protected.

So let’s summarize. Through decentralized databases (blockchains) we can replace centralized, proprietary databases. Thereby, users achieve self-ownership of digital assets, the right to permissionless innovate on the internet and the right of free access to information, data and assets. Understanding the original innovation, which was fundamentally just a new database, allows us to follow the development of blockchains and indicates what the future roadmap might look like. To understand the future roadmap of blockchains, we go back in time, revisiting the long-term trends in communication systems.

2. The Evolution of Communication Systems

Before diving into the history of communication systems, we want to thank Placeholder VC. Their theories on Crypto and communication systems in general are unparalleled and have allowed us to gain a deeper understanding of the Crypto space. Borrowing from Placeholder’s work, the history of communication systems is a multi-decade cycle of 1) Expansion driven by competition, 2) Consolidation/Monopolies driven by business models innovation and 3) Commoditization/breaking of monopolies driven through the emergence of new technologies. Expansion, Monopolies and Commoditization. Over and over again the cycle repeats.

Hardware Era

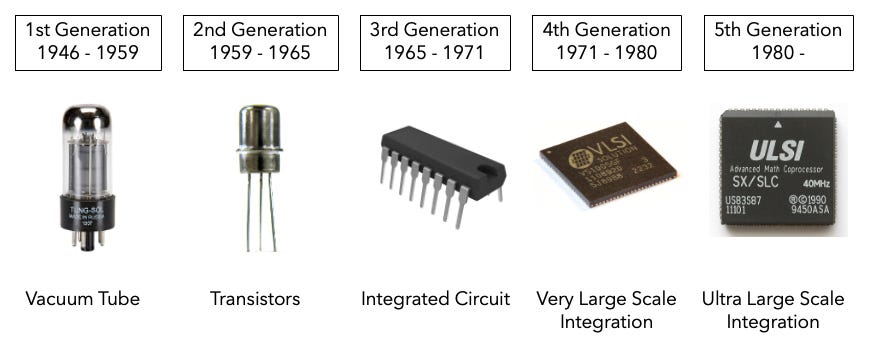

Going back 80 years, nobody (apart from the US and UK military) had computers due to the high cost barriers to entry. As computers relied heavily on vacuum tubes, they were very expensive to produce (due to lack of standardized manufacturing as the parts were very different). However, in 1947, the transistor was invented. The invention changed everything, over time breaking the first “monopoly” of computers. Artisanal-produced vacuum tubes were replaced by mass-manufactured transistors, leading to the collapse of production costs of electronics. Suddenly, it was economically feasible to build computers at a larger scale and sell them to small businesses rather than the military. Subsequently, the race to conquer the new market was opened. Over time, this new market would be consolidated by IBM.

Exhibit 6: Different computer generations had an impact on processing power (Moore’s Law)

In the 1970s, another new technology - the microprocessor (= integrated circuit) was produced for the first time commercially in 1971 - compressed the expensive, highly customized CPU systems into a single, general purpose processor that could be mass produced. Yet again, as the production costs for computers decreased, more companies emerged which started to build computers. New entrants meant more competition for customers, supply chain and talent, which consequently lowered the margins. As a result, IBM’s monopoly slowly broke down. Consequently, talent and capital was looking for another frontier to generate out-sized returns. Once again, a new technological innovation broke a monopoly.

Exhibit 7: The Placeholder theory of “Open standards and investment returns” is too important to ignore. Their theory explains the repeating cycles of expansion, monopolies and commoditization.

Software Era

As computers were slowly becoming more mainstream, a growing demand for new services (i.e.: operating systems) appeared - after all, customers also wanted to use their expensive computers. The initially strong competition within the operating system market eventually disappeared as Microsoft cemented its leadership position through business model innovation. Microsoft had locked in the market through its smart distribution strategy (accessing end-users through hardware vendors partnerships) and its superior product (proprietary operating software).

Only a few years later, once again, a new platform would come to eradicate Microsoft’s monopoly - Linux and the Web. Linux built the first, open source software operating system, offering users a new, highly customisable alternative to Microsoft Windows. Instead of buying the operating software via hardware vendors, users could just simply download the operating system through the internet - bypassing Microsoft’s Go-To-Market channels. Through this tactic, Linux not only accessed new customers but also managed to onboard Microsoft’s users who wanted to add more functionality. Once again, another monopoly broke down as the market became commoditised and the value of proprietary software diminished. Once again, talent and capital was looking for yet another frontier to generate out-sized returns. The new frontier was found within data networks.

Network Era

Within the past 15 years, through the increase in computing power, the cheaper costs of data storage, and the spread of data-collecting devices, the importance of big data grew. This gave rise to data networks such as TikTok, Facebook, Google, Amazon and Apple. By collecting large, uniquely valuable proprietary datasets, these networks build fantastic products, which locked-in users (i.e.: Cookies so we can conveniently surf the internet). As the networks are “owning/controlling” their users through their product lock-in and extensive market share (i.e.: Google has 93% market share in search), it has become almost impossible for competitors to emerge.

In addition, BigTech companies are continuously vertically integrating through offering new products, thereby getting more powerful as a result. For example, Google’s search offering has changed significantly in the past decade. While 10 years ago, Google would guide users to the websites, today, the relevant information is displayed on Google directly. As a result, users have no need to leave Google to access other websites. Although highly convenient, it increases Google’s monopolistic power over time. The fact that BigTech companies own their users, dominate different market segments and integrate vertically, has a profound impact on new entrants and product innovation.

Let’s look at a concrete example: It took Spotify 11 years and several billion USD to get to 50m paid subscribers. Meanwhile, it took Apple only 3 years to get to the same number as they simply offered their new service to its broad user base. Furthermore, Apple has used its (almost) monopoly on the phone and iTunes app market to exercise its power over potential competitors. For instance, in 2022, Apple blocked updates for Spotify users, resulting in Spotify accusing Apple of ‘choking competition’ with App store rules. How far can Apple go? What would happen if Apple forces iPhone users to use Apple Music by blocking Spotify? Where are the limits of BigTech companies? Clearly, centralisation adds convenience for users through cookies, targeted marketing and targeted search. However, we believe that benefits are outweighed by the many negative consequences such as less product offering and limited innovation.

How Blockchains will change data networks

Are we at the “technological” end of history as described by Francis Fukuyama for politics in 1992? Have we found our long-term status quo and equilibrium? Personally, we find this hard to believe. Looking at the past 80 years, we can see that many monopolies (IBM, Microsoft, Google) are increasingly weakened by the emergence of new technologies (transistors, microprocessors, Linux and the Web, Blockchain and Cryptonetworks). As new technological innovations reduce the cost of production, more new entrants come to market and start competing with established incumbents. This, in return, pushes down prices and decentralizes existing market monopolies - a cycle that continues to repeat, over and over again.

Going forward, we believe that Blockchains with open, decentralized databases will break the current monopolies of data networks, starting a new era of innovation and expansion. We believe that commoditization of information is just the next natural step to open-source everything. “Liberating” information and data will lead a new era of open, permissionless innovation.

The Impact of AI on Blockchains

Going forward, we believe that AI and Quantum Computing will provide further tailwind for Blockchain technology. For us, AI is excellent at taking information from databases and creating new, creative outputs. The richer the database, the better the model. In our view, a blockchain database with its superior inherent properties (the user owns its data and is able to monetise it) will replace the traditional database over time. As a result, blockchain databases will amass “richer” and “better” data. At the moment the types of information saved in blockchain ledgers are pretty simplistic (i.e.: who owns what, what was the transaction history) and not yet “extremely” interesting. However, as the quality and quantity of information written into blockchain ledgers grows, AI models will increasingly shift away from traditional databases to blockchain databases. Therefore, we believe that AI is powering new applications built on-top of blockchain, rather than being built on top of the proprietary databases of BigTech. As a result, we see clear synergies between AI and Crypto.

The Impact of Quantum Computing on Blockchains

As of now, no one can exactly predict which mathematical operations Quantum Computers will be able to execute. However, there is broad consensus that Quantum Computing will not render databases or data networks obsolete.

One certain effect will be its impact on security assumptions as Quantum Computing will force Blockchain networks to upgrade their security to be Quantum Computing resistant. This is why developer teams in Ethereum are working on Quantum-resistant proof systems called STARKs. In addition, the millions of distributed users will provide additional security layers for Blockchain, making it difficult for external actors to corrupt the network. Each block has a timestamp and a link to the previous block forming a chronological chain reinforced through cryptography, ensuring the records cannot be altered by 3rd parties. Therefore, technically speaking, Blockchains themselves should be relatively immune to hacking or, at least, provide significantly better security architecture than centralized legacy systems and databases. Current projections assume that it does not require millions to be spent on quantum computing to be able to break into legacy systems. Like with AI, we believe that quantum computing is forming a symbiosis with Blockchain Technology, rather than conflict.

Before diving into more details on Crypto Networks and their Technology Stack, we will look into the Web2 Internet Stack and how its structure makes it difficult for new innovation to emerge.

3. Web2’s “Fat” Applications and “Thin” Protocols

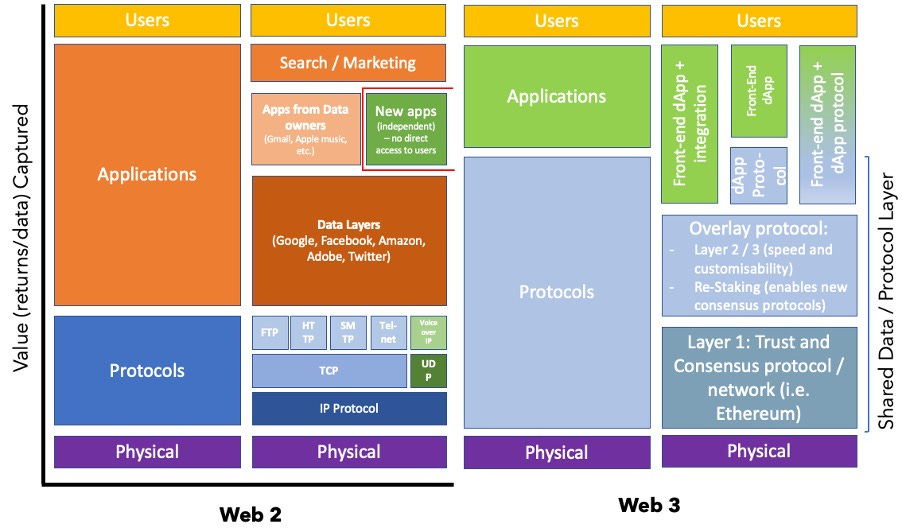

According to Joel Monegro’s Fat Protocol Thesis, today’s centralized Web2 and Crypto’s decentralized Web3 can be separated into 2 main layers - the Protocol Layer and the Application Layer. Within the Protocol Layer at the bottom of the stack, there are different protocols ensuring connection and data transmission. On the Application Layer at the top of the stack, there are different databases and applications, enabling users to interact with each other.

Exhibit 8: Value (data, investment returns, human talent) captured split between the Application Layer and the Protocol Layer

Web2’s Thin Protocols

The underlying internet protocols are not just a singular thing. They are a complex web of interconnected machines spanning the globe with different protocols that were built over time for different purposes. At the very bottom, there are the physical hardware layers consisting of computers. One layer up, we find the Internet Protocol (IP). Developed in the 1970s, the IP sends information packets to their destinations, while the Transmission Control Protocol (TCP) arranges the packets in the correct order. This is needed as the IP sometimes sends packets out of order to ensure the packets travel the fastest ways - similar to a postal service. As an alternative to the TCP, there is also the User Datagram Protocol (UDP) which also interacts with IP to transmit time-sensitive data. For example, UDP enables low-latency data transmissions between internet applications, ideally used for Voice over IP (VoIP) or other audio and video files. In practice, UDP allows you to look at videos even though not all packets have been transmitted.

On top of the TCP and UDP, there are different protocols for different use cases. For example, there is the File transfer protocol (FTP) which is used when a client (i.e.: a computer or a software) requests a file and the server supplies it. Furthermore, there is the Simple Mail Transfer Protocol (SMTP) which is a popular email protocol. In addition, we also find the Telnet, developed in the 1960s, which is designed for remote connectivity. It establishes connections between a remote endpoint and a host machine in order to enable a remote session.

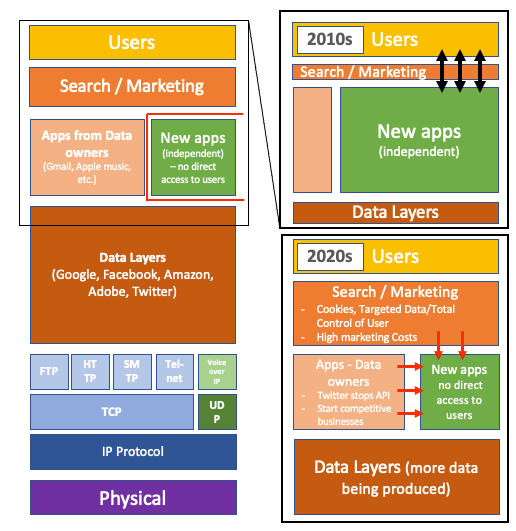

Due to their technicality and the fact that they have been built independently over many years, it is almost impossible to access the protocols without the convenience of front end user interface or user experience (UI/UX). As a result, many years ago, tech companies started to build applications so users could easily use their computers and the underlying protocols.

For example, one of the first popular applications allowed the user to listen to music on the computer. The user would insert a CD, copy the data to its local data storage and would be able to listen to music as it was stored locally. However, over time, users wanted to access data that is not stored on the local storage. This required a web browser to access non-local data. To stream a video on YouTube, the user would type in YouTube’s web address. The web address is then processed by the computer and sent - through a rather complex process - through an internet router into the web. After the request leaves the router, it bounces from router to router on a path to YouTube’s server. The request knows where to go based on a process that links the web address name to its server IP and MAC address (= its internet and physical location). Once it reaches YouTube’s server, the request to access its website is processed and accepted, with the data necessary to display the page accessed by the user’s computer. If the user searches for a video, the process is repeated. In fact, this process is used for pretty much everything accessed on the Internet. Over time, as data grew, locally-stored computers were converted to servers, purely dedicated to hosting and storing data in an efficient manner.

Web2’s Fat Applications

Parallel to the growth of physical data infrastructure, companies that built the original applications in Web2 started to equally built out the data storage infrastructure to capture an increasing amount of data. While the underlying protocols were open and could not be monetised, applications and their front-ends for customers could be monetised and could yield investment returns. As a result, most talent and investment ended up moving onto the application layer.

Over time, the applications started to vertically integrate by building their own data layer, thereby creating their own defense mechanism. The shared internet protocols (IP, TCP, UDP, FTP, HTTP, SMTP, Telnet, Voice over IP) produced immeasurable amounts of value by building connections on the internet (basically the roads within a city). However, most of the value got captured and re-aggregated on the application layer - notably by applications that started as web-page and vertically integrated to capture all data. This led to “thin” protocols and “fat” applications in Web2.

Over time - especially from the early 2010s until the early 2020s, big data players consolidated their stronghold in the industry even more. This was done through many different methods. Twitter for example stopped their open API used by companies to access users. Apple used its power position via the AppStore to reduce visibility of other, competing applications. Google has imposed illegal restrictions on Android device manufacturers and mobile network operators to cement its dominant position in general internet search. As the power of BigTech grew, it became increasingly difficult for new applications to access users. This has led to a situation where new applications are now trapped inside the BigTech universe. Accessing new users is not only difficult but increasingly expensive as the user’s attention is heavily controlled by BigTech and their products. This means that we have shifted towards a state where Big Tech is now a chokehold on innovation. Drawing on our history lesson (Evolution of Communication Systems), we now see how Big Tech has reached a state of (almost) complete monopoly.

Exhibit 9: Over time, Big Tech companies which are providing the data layer and have a close relationship to existing users (due to their popular apps) are increasingly expanding their own applications, becoming a chokehold to new applications.

As a direct comparison with the existing Web2 stack, we have also outlined the current Web3 stack (Exhibit 9). We believe that through Blockchain databases, the proprietary data layer can be opened and information can be “liberated/made public”. Open-sourcing data would reduce the chokehold of BigTech companies and lead to increased innovation. Overall, we believe that the relationship between protocols and applications is reversed in Web3. The majority of the value and data is concentrated at the shared protocol layer while a minority of that value is distributed along at the applications layer. This leads to a stack with “fat” open-source protocols and “less fat” applications and data layers.

In order to understand how Blockchain technology broke this data monopoly and led to permissionless innovation, we need to understand how Bitcoin and Ethereum built trustless networks.

4. The Evolution of Layer 1s - Bitcoin, Ethereum, Modular Blockchains and Eigenlayer

Enter Bitcoin

With the Bitcoin whitepaper in 2008, the concept of decentralized trust was born. In Web2 users had to trust tech companies for data handling (i.e.: Google’s motto “Don’t be evil”) and that previously agreed-upon rules remained in place. In contrast, Web3 protocols are built on open-source code, cryptographic rules (= rules cannot be altered), and public blockchains with public verifiability. As every action is a result of code, users can verify themselves if the code has executed the operation as intended. As a result, the Web2 model of “Don’t be evil” has been replaced by the code-based Web3 model of cryptographic rules following the premise of “Can’t be evil”. Through this evolution, decentralized trust (= not having the need to trust a single party) was born. How did Bitcoin become a trustless network and what makes it special?

“Because unlike any other tool for sending money over the internet, Bitcoin works without the need to trust a middleman. The lack of any corporation in-between means that Bitcoin is the world’s first public digital payments infrastructure. By public I mean - available to everyone and not owned by any single entity. We have public infrastructure for information, for websites, for email - it is called the internet. But the only public payments infrastructure that we have is cash/FIAT - and it only works in face to face transactions. Before Bitcoin, when you wanted to pay someone remotely over the phone or the internet, you could not use public infrastructure but you had to rely on private infrastructure (bank) to open their books and add a ledger entry that debits you and credits the person you are paying [Basically moving information from the database of your local bank to the database of the receiver bank - with 2-8 different banks in between]. With Bitcoin, the ledger is the public blockchain and anyone can add an entry to that ledger transferring their bitcoin to someone else. And anyone - regardless of their nationality, race, religion, gender, sex, credit worthiness, anyone can for absolutely no cost can create a Bitcoin address in order to receive payments digitally. Bitcoin is the world’s first, globally accessible money. [...] If we can replace private payments infrastructure, then we can replace other private chokepoints to human interaction as well [referring to Ethereum’s quest to build a decentralized supercomputer]”

So why are many stakeholders building more public infrastructure similar to what Bitcoin did in the digital payments infrastructure? Because over time, intermediaries providing today’s critical, private infrastructure are becoming fewer, larger and more powerful. This aspect of centralisation and monopolistic positioning hinders innovation and progress.

Bitcoin’s trust status

How did Bitcoin achieve this “Trust Status” and how did it become accepted as a trusted public payment infrastructure for transactions between different stakeholders?

Bitcoin's “Trust” pyramide consists of a Decentralized Trust Layer on the bottom, a Consensus Layer in the middle and an Application Layer on top. So let’s explain by starting in the middle.

Exhibit 10: Bitcoin’s “Trust” pyramide/stack

Consensus between the many thousands (decentralized) members of the network is reached through a method called Proof-of-Work (PoW). While Bitcoin uses PoW as a consensus mechanism, there are many different methods to reach consensus such as Ethereum’s Proof-of-Stake (PoS) or Solana’s Proof-of-History (PoH). In PoW, members (= computers) of the network, called Miners, compete against each other to solve difficult mathematical puzzles. The puzzles are difficult to solve, but it is easy to verify once the correct solution has been found. Once a miner has found the right solution, they are allowed to build a block (= a new entry to the database recording the new state of the database). The miner then sends the solution to all other members, who verify that the solution is correct. If the solution is correct, the block is added to the blockchain and the miner receives a block reward. Bitcoin has an inflation rate of 1.7% per annum as they are issuing new blocks to the miners, who then sell the block on the market to cover their electricity and hardware expenses. Through mining, the community members (= decentralized trusted parties) reach consensus on the new state of the blockchain through PoW (= a method to reach consensus = consensus method).

On top of the Consensus Protocol, there is the Execution Layer. The Execution Layer defines which operation(s) can be executed with the protocol. For example, within Email, the only operation that can be executed is sending emails - one is not able to purchase goods online or transfer money. With the Bitcoin protocol, the only operation that can be executed is the transfer of Bitcoin tokens (BTC). BTC is the native asset to the network, just as USD is the native token asset of the United States. In the transaction process, one user wallet initiates the transaction, which is then executed through the Bitcoin protocol. A miner is chosen via the PoW consensus, builds a block in which the transaction is included, and adds the block to the blockchain. This results in a new consensus of the latest status/state of the database.

As the Bitcoin network relies on a Decentralized Trust Layer with no centralized party and facilitates the exchange of BTC, the Bitcoin protocol has become the first public payment infrastructure. As the only operation that can be executed is the transfer of BTC, Bitcoin is also known as a single-application network.

However, over time, developers envisioned more applications (= operations that can be executed on the network) which could be built relying on Bitcoin’s revolutionary idea of decentralized trust and global consensus. Nonetheless, because Bitcoin was a single- application protocol, none of those applications could be built on top of Bitcoin’s Trust and Consensus layer, representing a significant barrier to innovation. As a result, more and more single-application networks were built consisting of their own Decentralized Trust Layer, their own Consensus Layer and their own single Application Layer. Although the code was open-source and could be easily copied (= forked) with different applications, the heart of Bitcoin - its community willing to secure the network (= the Trust Network) - was not easy to duplicate. Bootstrapping a Decentralized Trust community, which is securing the network, was not only extremely expensive, but also difficult to do. Thus, the missing flexibility of Bitcoin’s single-application network represented a clear barrier to innovation.

Exhibit 11: Bitcoin and Ethereum are both Trust Networks. While Bitcoin is a single-application blockchain for the transfer of the Bitcoin Token (BTC), Ethereum has built a Turing-complete machine on top of its trust network. This allowed anyone to build decentralized applications on top, thus making Ethereum a multi-application blockchain

Enter Ethereum

Due to the single-application nature of Bitcoin, many developers envisioned building a multi-application blockchain, which was created in the form of Ethereum. With Ethereum, three main innovations emerged:

First, Ethereum replaced the original Bitcoin script, which only limited the network to executing solely a single application, with a Turing-complete-machine. A Turing-complete machine is a machine capable of solving any problem using a predefined set of rules to determine a result from a set of input variables - in short, a computer. Located on top of the consensus protocol, Ethereum’s Turing-complete machine allowed developers to build more applications. This transformed Ethereum into a multi-application protocol offering a highly demanded alternative to Bitcoin’s single-application protocol.

Second, to automate applications and transactions, Ethereum created Smart Contracts (the definition comes later). Rather than having to manually start transactions, suddenly users and developers could automate (trans)actions. With the creation of Ethereum, the industry moved from Bitcoin’s distributed ledger (i.e.: Address bc1qx…y2 owns 0.43BTC) to a fully virtual computer that could automate and execute more operations. The right real-world analogy would be to compare the email system (Bitcoin) with the internet (Ethereum).

Third, as a result of the first two innovations, Ethereum allowed the creation of different token types. Tokens are defined as digital assets living on the blockchain, representing achievement badges, a medium of exchange, or proof of membership. Off-chain (= in the real world), different achievements have different properties. For example, there are indistinguishable goods such as banknotes, but there are also unique goods such as paintings or contracts. Through creating tokens with different properties (ERC-20 for money, ERC-721 for NFTs/unique assets), Ethereum allowed users to represent the off-chain world on the blockchain. This meant that users could finally build ownership of digital assets.

Creating a Turing-complete machine reduced barriers to innovation

Replacing Bitcoin’s script with a Turing-complete machine (= a globally distributed computer) kick-started innovation. Rather than having to go through the expensive and tiresome process of bootstrapping a new Trust Network (costing >$20m) to build a single application, developers could simply code applications on top of the Ethereum machine. As this new layer was added, it decoupled trust and innovation. The cost of creating a Trusted Network moved to zero as applications could suddenly rely on Ethereum’s Trust Network and focus solely on building great applications. As a result, the cost of new innovation decreased significantly, leading to more innovation. Suddenly, anyone could build applications on top of Ethereum’s Trust and Consensus Layers and be assured that the transactions are included in the public database ledger.

Creating Smart Contracts

Smart contracts are computer programs stored on a blockchain that run when predetermined conditions are met, following the idea of “If action A happens, action B happens auto- matically”. Through the application of smart contracts, one removes the need to trust multiple parties in the process of buying or doing something. Rather than having to trust a third party that action B happens, users know that action B happens automatically. As a result of smart contracts, dApps (decentralized applications) were born. dApps are applications that run using smart contracts for automation on top of a decentralized network. Rather than needing to trust a middleman to execute actions, actions of any kind could now be executed automatically through code.

Creating different token properties

The Bitcoin blockchain (= decentralized database) could only store information related to the Bitcoin token (i.e.: Address bc1qx…y2 owns 0.43BTC). While this represents an outstanding innovation in terms of decentralized database design, it had its limitations in terms of real-world applicability. As mentioned, in the off-chain world there are billions of different information types. For example, there are indistinguishable data points or assets such as monetary assets such as banknotes which can be represented with Ethereum’s ERC-20 token type. However, there are also unique elements like contracts of paintings. On-chain those can be represented with the ERC-721 token. Allowing to bring real-world assets to the on-chain world while keeping their unique properties, increased the usability of the network. As a result, every data point could be represented on the blockchain.

In conclusion, by adding a new computing layer, Ethereum split innovation and trust. Suddenly anyone could cheaply build applications on Ethereum’s Trust Network, reducing the cost of innovation dramatically. Due to the open nature of the network, anyone could build - a textbook example of permissionless innovation. By creating smart contracts, Ethereum enabled new forms of automated applications. By creating different token types, it created the opportunity to represent any off-chain asset on Ethereum’s decentralized supercomputer.

How Ethereum’s machine works

To understand how the Ethereum machine runs - specifically how it creates blocks and executes transactions - one needs to understand the respective layers. Comparing to Web2, we continue to split the stack between protocols and applications. For now, we only consider the Monolithic-version of Ethereum - basically looking at the case where everything is done “in-house”. Later on, we will also look at modular versions of the blockchain where some or more layers are “outsourced” for technical (scalability) reasons.

All of Ethereum’s other layers are built on top of its Trust Network. Ethereum’s Trust Network consists of ~11600 nodes and ~500k validator nodes. A node is a computer in a Peer-to-Peer network which simply maintains a view of the beacon chain and shard chain. Validator nodes actively mine and validate new blocks in Ethereum’s PoS Consensus system and are responsible for storing data, processing transactions, and adding new blocks to the blockchain. A node can run several validator nodes. Each validator node runs two types of softwares (= clients): the Execution client and the Consensus client. Ethereum relies on a multi-client architecture to increase security and vitality. Suppose a defect is isolated to a single client. In that case, the network can continue to operate because other nodes running unaffected clients will manage the network while the impacted nodes switch to another, unaffected client. Before exploring the functions of the other layers, let’s look at their interoperability in a concrete example.

Step 1: A transaction happens. For example a user sends a token or triggers a Smart contract in an exchange dApp to swap ETH with BTC.

Step 2: The transaction is submitted to an Ethereum Execution Client (= one of the softwares running on the validator nodes). The client then verifies the validity of the sender (i.e.: Does the sender have enough ETH to encourage everyone to include the transaction in the next block?)

Step 3: If the transaction is valid, the Execution Client adds it to its local “mempool” (= short for memory pool). The “mempool” contains a list of pending transactions.

Step 4: Of all the ~500k validator nodes, one validator node is selected randomly - thereby becoming the block proposer node - to build the block and broadcast the next block to the network. As a next step, the Execution Client of the node bundles transactions from the “mempool” into an "execution payload" and executes them locally to change the status of the blockchain (= state change). The information is passed to the Consensus Client of the node where the new block is created.

Step 5: Other nodes receive the new block on the Consensus Layer “gossip” network. The other nodes then pass the new block to their Execution Client. Within the Execution Client, the transactions are downloaded and re-executed locally to ensure the proposed block (who changes the state of the blockchain) is valid. If the block is valid, it reaches finality (= it becomes part of the blockchain and cannot be changed) - basically the blockchain has reached a new state. On another note, in its monolithic state, Ethereum is currently only able to achieve ~8-15 transactions on average. The reason is that each Execution Client needs to download the full transaction data and re-execute the block.

Exhibit 12: Ethereum’s layers split between protocol vs. application layer

Several layers are required to operate with each other to include a transaction in the Ethereum blockchain and to change the latest state of the blockchain. Let’s look at each of the layers.

Trust Network: On the base layer, there are physical nodes (nodes = computer in a Peer-to-peer network). Within the Ethereum network there are three types of nodes - nodes that can propose blocks (Full nodes), nodes that cannot (Light nodes) and nodes (Archive nodes) that store a history of Ethereum’s states (i.e.: state at time t, state at time t+1). For simplicity reasons, this report will talk about Full nodes when talking about nodes. A Full node can run several validator nodes - which explains why ~11600 Full nodes on the Ethereum network can run ~500k validating nodes. As mentioned, each Full node runs two softwares (clients): the Execution and the Consensus client.

Full nodes: Full nodes can run several validator nodes, which propose and verify blocks, therefore earning protocol rewards (~6% APY paid in ETH token). One Full node (= computer in a Peer-to-Peer network) can run several validator nodes (= smaller computer that runs two software clients). Due to the responsibility, the Ethereum network requires economic commitment which means that validator nodes need to commit (= stake) 32 ETH (~$52k). If the node or their software behaves maliciously, the validator node operator gets punished and loses part of its stake - this process is called slashing.

Light nodes: While the Execution client of Full nodes downloads every block (see #5), Light nodes only download block headers which contain only summary information about the contents of the blocks. Light nodes enable users to participate in the Ethereum network without powerful hardware or high bandwidth required to run Full nodes (i.e.: on the phone). As Light nodes are not downloading all the block data, they do not participate in consensus finding as validators (see #5).

Archive node: Archive nodes build historical states. Those nodes are needed if an application wants to query a concrete state in the past. Archive data represents units of terabytes, making archive nodes less attractive for average users. However, they can be useful for services like block explorers, wallet vendors, and chain analytics.

Consensus Client: The Consensus Client receives the proposed block from the Execution Client. Thereby, the Consensus Client downloads all transactions from the newly proposed block. Afterwards, it re-executes the transactions to confirm compliance with consensus rules (basically validating/attesting the block). Once re-executed, the Consensus Client shares the block with the Execution Client who then itself shares it with the broader network.

Execution Client: The Execution Client software listens to new transactions broadcasted in the network (EVM) - for example someone triggers an automated Smart contract or transacts a token. As a first step, the Execution Client verifies that the transaction is possible (i.e.: Can the sender pay the network fees?). Once verified, it sends the transaction to the “mempool”. This process of finding new transactions, verifying its validity and sending it to the “mempool” is done by all Execution clients of all Full Nodes/validator nodes.

Every couple of seconds, a new validator node is chosen by a random algorithm to build a block. In this case, the Execution Client (of this specific node), bundles the transactions together into a block and sends it to the Consensus Client. Once the Consensus Client attests (= confirms) the block, the Execution Client then proposes it to the network.

As all the other validator nodes receive the proposed block and their respective Execution Client downloads the transaction data and re-executes the transaction. If the execution is correct, all the other Execution Clients agree to a new (changed) state of the blockchain.

Concludingly, this means that Execution Clients have the following tasks: First, they listen to transactions in the network and add them to the “mempool”. If their Full node/validator node is the new block proposer, their Execution Client proposes blocks by bundling transactions. If their Full node is not the block proposer, they download the transaction data, re-execute the transaction and verify the suggested block.

Data Availability Layer: The core tasks of blockchains include executing transactions (done via Execution Clients), achieving consensus on transaction ordering (done via Consensus Clients), and guaranteeing the availability of transactional data to all nodes on the blockchain. Data availability is important because it allows nodes to independently verify transactions and compute the blockchain’s state without the need to trust one another.

The current scalability issues are coming from the requirement of the Execution Client to download and verify data, which reduces throughput (= low transactions per second). In addition, using on-chain storage for an increasingly large amount of information limits the number of entities who can run Full node infrastructure, which leads to centralisation risk if only expensive computers can run nodes. Making data available as the Ethereum Blockchain grows is one of the challenges of the network.

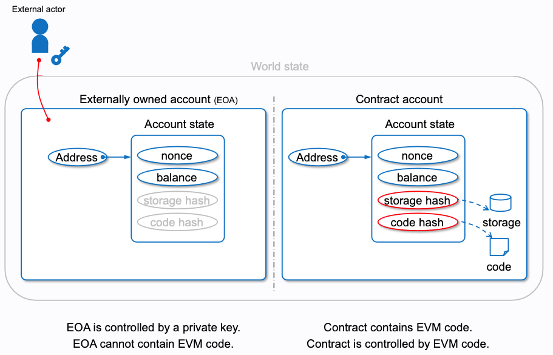

Turing-complete machine/Ethereum Virtual Machine (EVM): Bitcoin’s data structure consists of accounts (Address bc1qx…y2) and balances (0.43BTC). If a user wants to change the state of accounts and balances, they need to initiate a transaction. In contrast, Ethereum not only has Peer-to-Peer transactions but also uses automated smart contracts in its applications. While transactions are initiated by the owner, smart contracts (which are based on open-source code) are run by the Ethereum Virtual Machine (EVM). The EVM is a computation engine that is in charge of deploying and executing smart contracts, and updating the state for every new block added to the Ethereum blockchain. Conceptually, the EVM is a piece of software that sits on top of the node infrastructure of the blockchain and performs critical functions such as running code used for dApps and Smart contracts. By being positioned between the nodes and the smart contracts, the EVM can compile different kinds of smart contract code into a standard format known as bytecode. This code makes the smart contracts readable by the Ethereum network and therefore enables those transactions to be recorded by the Ethereum nodes. This guarantees that dApp data is included in the blockchain. Think of it like being the logistics service that runs the errands between smart contracts and users, making sure that all transactions are included. As mentioned above, by creating the EVM, Ethereum developers can build on top of it - and are not required to build their own trust network.

Application protocols: A protocol is defined as a set of predefined rules (run by the EVM) that dictates how a blockchain operates. It also defines the rules, which all network participants must follow so that the blockchain can function. As a result, application protocols are systems of rules that allow applications to run on the Blockchain. Most applications have their own decentralized application (dApp) which is the part users interact with through the User interface (UI). However in theory, one can interact with the open-source protocol without the UI by learning the programming language - something that is never done in practice. Having great UI/UX is essential for protocols to attract users. For example, let’s say a lending protocol like Aave does not have a UI. Its liquidity would be gone in an instance, because the vast majority of people would not bother learning a programming language to access it.

decentralized Applications (dApps): dApps are website UI that connect the user’s browser with the underlying protocol, its smart contracts, and algorithms hosted on a blockchain network. In other words, the protocol can exist without a web interface, while the web interface would not be useful without the protocol. As most protocols are open-source, in theory, anyone can build their own dApp on top of an existing protocol. For example, in August 2022, Office of Foreign Assets Control (OFAC) of the U.S. Department of the Treasury blacklisted Tornado Cash, an open-source privacy protocol which allowed users to obscure the trail back to the fund's original source. Any public address (i.e.: x0382…273) that has been using the service was blocked from using the front-end of other dApps (such as Uniswap). However, as Uniswap is a permissionless protocol, blocked users could still use the underlying protocol through the code base. While the dApp belongs to an organization, the underlying protocol code is free and can be used by anyone.

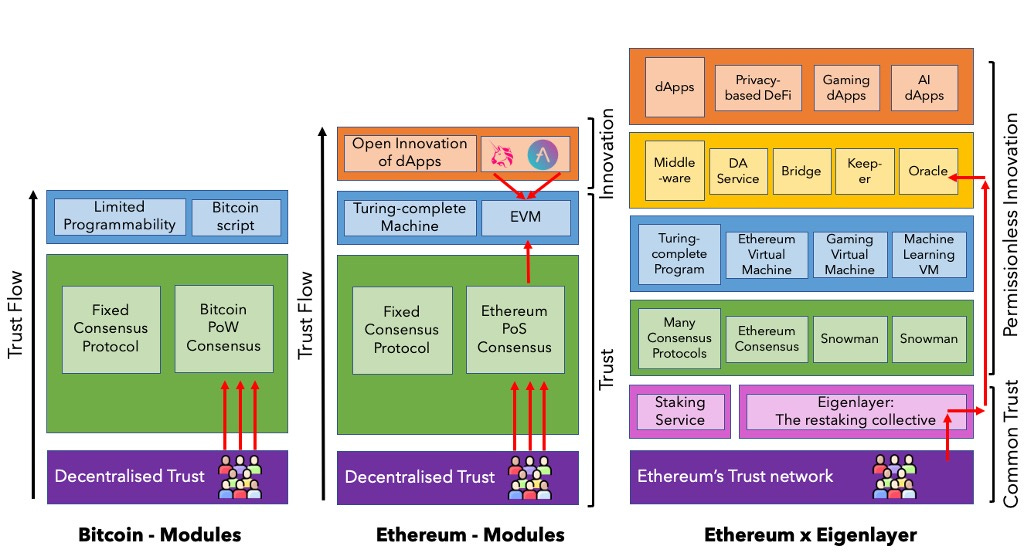

Modularisation of Blockchains

Up until the emergence of Ethereum in 2014/2015, only single-application Blockchains - such as Bitcoin, Filecoin and Namecoin - existed. With Ethereum, the first “quasi-modular” blockchain was developed. This was achieved as Ethereum replaced the original Bitcoin Script with its own Execution Layer, thus splitting innovation and trust. This modularisation of innovation reduced the costs of innovation significantly as there was no need to bootstrap the expensive Trust Network and stakeholders could just build on Ethereum’s Trust Layer (= its ~11600 Full nodes and ~500k validator nodes) and Consensus Layer. However, Ethereum itself has remained a monolithic blockchain as it has kept the Consensus/ Settlement Layer, the Execution Layer and the Turing-complete machine inside its stack.

However, what happened if developers wanted to have even more modularity? For example requiring a different consensus mechanism to deal with faster block finality. Or for building applications that require more data points which are less sensitive (i.e.: social media app)? Or using a completely different virtual machine to power more gaming applications? As the list of potential use cases grew, it became apparent that Ethereum’s “fixed”, monolithic stack infrastructure had reached some limitations. Ethereum had built the strongest Decentralized Trust Layer powering the biggest and most trusted Global Consensus machine - but what if an application (i.e.: a game) does not need global consensus but just in-game consensus?

Once again, the problem repeated itself. If developers wanted to have more modularity, they had to bootstrap their own Trust Network and adjust Consensus Layer and the Virtual Machine for their respective purposes. As a result, Ethereum’s limitations gave rise to more modular Alternative (Alt)-Layer 1s in 2018/19. Over the next few years, many new Trust Networks appeared with vastly different properties (around Execution Layer, Consensus Layer, Settlement Layer and Data Availability Layer) allowing developers to create novel products. Let’s recap the different layers:

Execution Layer: Provides an environment for dApps and processes their transactions.

Consensus Layer: Determines the sequence of transactions. Inside Ethereum, Consensus is achieved through PoS (Proof of Stake - basically people use their ownership stake to vote - in case of bad behavior, ownership is reduced), while the Bitcoin network uses PoW (miners compete to solve a mathematical equation). The Consensus Layer agrees on the contents and ordering of transactions.

Settlement Layer (usually combined with Consensus Layer): Provides a layer for finalizing transactions, settling disputes, validating proofs, and bridging between different execution layers.

Data Availability Layer: Nodes receive a block from a block producer and check if the data (transactions) is publicly available. Basically, the DA layer guarantees the availability of transaction data.

Monolithic blockchains are blockchains that handle all three components (execution, consensus/settlement, data availability) of the modular stack - for example Ethereum or Bitcoin. On the contrary, modular blockchains are blockchains that outsources at least one of three components to an external blockchain or handle the component locally. Due to the modular design, blockchains have become more flexible in design principles. This flexibility also allows modular chains to be easily created, mixed, or replaced independently within a modular stack. Just like Lego bricks, modular blockchains can be independently created for each use case.

This flexibility meant that for the first time in the history of blockchains an application can pick its infrastructure according to its technological needs - and does not need to refrain from building more functionality as the underlying technology cannot support it. As each component can do only a few things, the modular blockchain must do them very well. This allows developers to create their own blockchain stack suited to their novel application.

Exhibit 13: While Ethereum started as a monolithic blockchain, over time it has started to become more modular (with the help of roll-ups) depending on the use case. Newer modular blockchains like Celestia started with the initial idea of modular blockchains.

There are many different types of modular stacks. For example Ethereum started as a monolithic blockchain, but has become more modular with the help of roll-ups. Thereby, the network has moved towards a roll-up centric roadmap to solve its scalability issues.

Ethereum’s Scalability Issues and the Blockchain Trilemma

As a recap, a blockchain is a distributed database where blocks of data are organized in chronological order. The basic idea is that with the help of decentralized blockchains, users do not need to rely on trusting third parties for networks and markets to function. In order for this to be achieved, a blockchain needs to have 3 major properties: security, scalability and decentralization. However, as blockchain technology is increasingly adapted, the blockchain should be able to handle more data at faster speeds so that using the network does not become too slow or too expensive to use. Popularized by Ethereum’s co-founder Vitalik Buterin, the Blockchain Trilemma refers to the idea that it is difficult for blockchains to achieve optimal levels of all three properties simultaneously as increasing one usually leads to a weakening of another. We will use Ethereum as an example to understand its scalability boundaries and how it is using roll-ups or modular blockchains to solve them.

Exhibit 14: If blockchain technology is to be adopted globally, it should be able to handle much more data, and at faster speeds, so that more people can use the network without it becoming too slow or expensive to use. However, the fundamental design of many decentralized networks means that increasing scalability tends to weaken decentralization or security. This is what’s known as the blockchain trilemma (Binance).

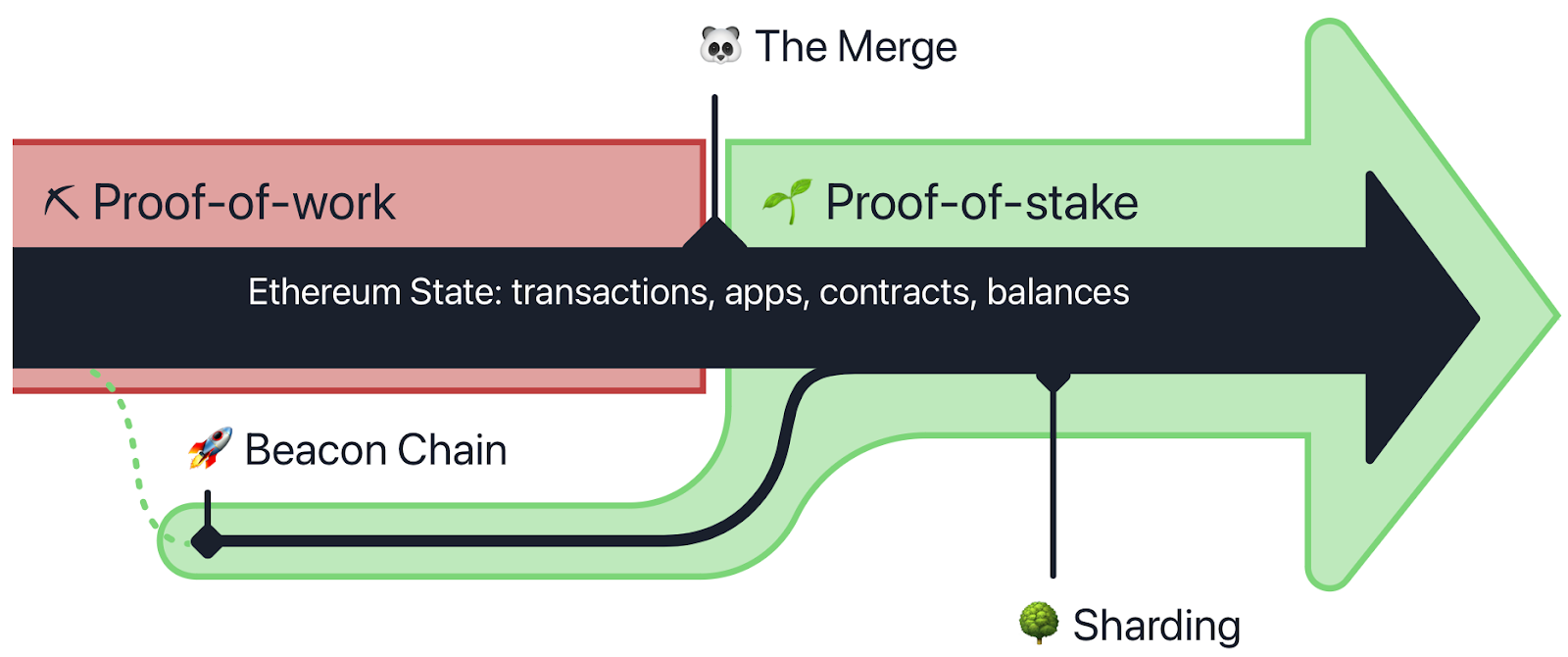

On the security aspect, Ethereum is considered one of, if not the most secure network. Through the Merge in September 2022, the network has moved from PoW to PoS which has added additional economic and technological security. Relying on ~11600 node operators and ~500k validators all around the world, currently 16.3m ETH (~$25bn) are staked as of January 2023. In order to attack the network, the potential attacker would need 51% of the staked ETH (~12.5bn). With 51%, the attacker could then use their own voting power to ensure his “copy” of the database would be used for future block building, which would render the “old database” and its values worthless. However, apart from being economically infeasible (as the price of ETH would increase drastically with new inflows in the billions), the switch from PoW to PoS gives the community additional flexibility in mounting a counter-attack. For example, the honest validators could decide to keep building on the minority chain (aka the “old database”) and ignore the attacker's fork while encouraging apps, exchanges, and pools to do the same. They could also decide to forcibly remove the attacker from the network and destroy their staked ETH. These are pretty strong economic defenses against a 51% attack. Against other attacks, the Ethereum network has other proposed solutions (here). For reference, it would cost an attacker $951,552 to hijack the Bitcoin network for 1h as it is relying on the different consensus algorithm PoW.

On the decentralization aspect, Ethereum is also considered to be top of its class. Ethereum is currently run on 508,000 validator nodes on ~11600 computers with 43% being located in the US, 12% in Germany, 4.5% in Singapore and 4.1% in the UK. On the client's side, Ethereum is relying on a wide range of consensus client software (40% Prysm, 35% Lighthouse, 19% Teku), while having some centralisation issues on the execution client software (69% Geth, 14% Nethermind, 10% Erigon).

On the scalability side, Ethereum’s limitations have become obvious during the latest bull market, where users had to pay sometimes >$200 in order to conduct a transaction - clearly too much as Ethereum aims for transaction costs <$0.05. On a monthly average, Ethereum allows for 12 transactions per second, clearly too little for Ethereum’s aim to become the world’s global settlement layer. The main reason for its scalability issues is that every Execution Client (from every validator node) has to download the full transaction data from the proposed block before verifying it. While downloading and re-executing data limits scalability, it ensures that every block includes only valid transactions making the network extremely secure. In addition, keeping data open and downloadable is a fundamental property of the Ethereum blockchain. This means that moving from an open-source nature to a closed-source nature is not possible as everyone can download, thus having access to the underlying Ethereum data. In order to create the large-scale decentralized service Ethereum envisions, the protocol must allow anyone who downloads the software and the database to become a node and download a copy of the database. This is the reason why the Data and Consensus Layer of Ethereum can not be “made” proprietary such as their respective counterparts within the Web2 stack.

However, it is precisely because of this security mechanism of the Execution Client that Ethereum runs into scaling issues. Since Full/validator nodes download and re-execute every transaction to verify they follow the rules of the blockchain, Ethereum cannot process more transactions per second without increasing the hardware requirements of running a Full/validator node: Better hardware ⇒ create more powerful Full/validator nodes ⇒ Full/validator nodes can check more transactions = more scalability ⇒ bigger blocks with more transactions in it. However, as the hardware requirements of running Full/validator nodes increases, it would lead to a lower number of Full/validator nodes, thus reducing decentralization. This would mean that Ethereum is less secure as fewer people check the work of block builders to keep them honest. Voila, the Blockchain Trilemma has once again appeared. In order to solve the Blockchain Trilemma, Ethereum has moved towards a roll-up centric roadmap with many developer teams around the world actively working on roll-up solutions to increase scalability.

Exhibit 15: Ethereum is using its roll-up centric roadmap to solve its scalability issues

Roll-ups aim to combine scalability with the security and decentralization of Ethereum. Thereby, roll-ups execute the transaction outside of the main Ethereum network but post the transaction data back to the Ethereum network, thereby still deriving its security from the Ethereum protocol. In practice, roll-ups execute the transaction off the chain mainly on a rollup specific chain (= their own execution layer). Afterwards, the roll-up compresses the transaction data and sends it back to the Ethereum chain as it relies on Ethereum’s consensus and security derived by its global trust network - this means that the data from the roll-up will be taken into Ethereum’s Consensus Layer. There are several types of different roll-ups: Enshrined roll-ups (i.e.: zkEVM) and Smart Contract roll-ups (i.e.: Optimism, Arbitrum) for the execution layer, Smart Contract Settlement roll-up (i.e.: L2 Starknet) with its own Smart Contract Recursive roll-up (i.e.: a game-specific L3), Sovereign roll-ups and Validiums (i.e.: Immutable X). For more detail, we recommend Jon Charbonneau’s The Complete Guide to Rollups. We also provide deeper insights into Ethereum’s roll-up solutions on page 58.

One of the most exciting new developments within Ethereum is EIP-4844 (Ethereum Improvement Proposal) called Proto-Danksharding. With this update, roll-ups will be able to data post bundles under a new transaction type instead of using the current "calldata" (= storage which persists on-chain forever). The new transaction type will carry a blob, basically a large amount of data - inaccessible by the execution layer - which is much cheaper than calldata. Blobs are 10x larger than blocks, but they are pruned out of the blockchain after some time. This means that a new data-availability layer will arise (think like servers that can provide data when needed). As a result, the scalability of Ethereum increases by an order of magnitude.

Eigenlayer - Securing Middlewares & Alt-1s with Ethereum’s Trust Network

Barriers to innovating middleware protocols

Let’s assume there is a developer team and they want to create their own application. As their application is built on Ethereum, they can rely on Ethereum’s Trust Network. This means that they can be sure that Ethereum’s network will continue to process the app’s transactions and include those in the blockchain. For that service, the application will have to pay some gas fees to Ethereum and its trust network. Due to Ethereum’s recent transition from PoW to PoS, Ethereum’s block making service is extremely secure as ~$26bn of ETH is staked at the moment and attackers would need at least 51% (~$13bn) to manipulate the network. Basically, the app developers can trust Ethereum’s service that their transactions are included in the Ethereum database.

However, in order to run their dApp the developer team also need other middleware protocols which are providing services such as Oracles (data feeds that bring data from off the blockchain data sources and puts it on the blockchain for smart contracts to use), a Data Availability layer (storing the data the app produces) or Bridges (allowing data and crypto asset transfers across different chains). Rather than building all of those services by themselves, application developers can rely on existing middleware providers for those services - just like they relied on Ethereum’s block making service.

However, existing middleware providers face a micro-economic problem. Like every blockchain in 2015, middleware protocols face the same problem in 2023. In 2015, applications had to bootstrap their own trust network as they could not utilize Bitcoin’s trust network due to its single-application nature. This all changed with the development of Ethereum - suddenly applications could use Ethereum’s trust network for their own applications. However, middleware protocols are still required to bootstrap their own trust network - even in 2023. This means that every middleware protocol has to create their own trust network before building out its services.

For example a middleware protocol that provides data storage would need to build their own incentive program to make it economically unsustainable for a 51% attacker to hijack the network. This is called bootstrapping a Trust Network. One way would be to issue a token and provide token holders with a staking mechanism. Users who provide the service of storing data correctly receive more tokens, while those who behave maliciously lose their tokens - similar to Ethereum’s PoS consensus mechanism. In order to fend off attackers, the middleware protocol would need to aim to achieve the highest economic security possible. The reason is that higher economic security (i.e.: higher market cap of the protocol) makes it more costly for attackers to acquire 51% of the token supply, hijack the network and harm the protocol. While there are many ways to achieve high economic security, the most common method is to reward stakers (who secure the network) with more and more tokens. This method works very well in a bull market as token prices rise and the protocol archives higher economic security. However, in a bear market, additional token inflation leads to more supply on the market resulting in even faster dropping prices and lower economic security. In addition to being expensive, bootstrapping a trust network for a middleware protocol is also time consuming, requires a different skill set and is clearly a distraction for middleware developers whose job it is to build a novel middleware application.

Switching back to the point of view of the developer team and the dApp. The developer is relying on the “Gold standard “Ethereum for block making security (secured by ~$26bn, cost of corruption is $13bn) while also relying on several middleware protocols with significantly lower security (i.e.: data storage protocol secured by $1bn). Despite relying on the highest block making security assumptions on Ethereum, the application’s minimum security assumption is $1bn from the data storage protocol, representing a clear security risk for the application.

Exhibit 16: Bootstrapping a secure validator network is difficult and expensive, so middleware protocols can use EigenLayer to tap into the Ethereum validator network

Enter Eigenlayer

In late-2022, we saw the emergence of Eigenlayer, which built a mechanism to leverage an existing Trust Network to “do other things it was not designed to do” - basically following Ethereum’s playbook of 2015. In 2015, Ethereum allowed applications to use its Trust Layer. In 2023, Ethereum allows middlewares to use its Trust Layer through Eigenlayer’s protocol.

More detailed, Eigenlayer is a 2-sided marketplace which leverages Ethereum’s Trust Network and connects it with middleware providers (Oracles, Bridges, etc.) who are looking for additional security. In practice this means that Eigenlayer allows Ethereum stakers to “re-stake” their invested capital. Ethereum stakers commit to additional slashing conditions to provide additional services that are being built on Eigenlayer (oracles, bridges, data availability layer, new consensus protocol, etc.). In exchange, Ethereum’s stakers also receive additional yield (in addition to the ~6% APY they receive from Ethereum at the moment). This means that Ethereum’s stakers, who are securing the network and proposing and validating new blocks, can use their economic power to secure additional middleware such as oracles, bridges, sidechains or other consensus protocols. For Ethereum stakers this means that they can receive additional yield (up to 2-3x the current yield), while for other middleware providers this means they can receive trust through Ethereum’s trust network. As a result, middleware providers have no need to (costly) bootstrap their own trust network, which will lead to more innovation on the middleware layer.

Once again, the trend of further modularisation continues: In 2015, Ethereum modularised trust and innovation by building an operating system instead of the Bitcoin script, thus enabling the cheaper development of applications. In 2018/19, Alt-L1s further modularised trust and innovation by bootstrapping their own (weaker than Ethereum’s) Trust Networks to build customized consensus protocols and operating machines for more use cases. In 2023, we will see the best of both worlds: Merging Ethereum’s Trust Network and Alt-L1’s highly customisable Consensus Protocols and operating machines. How does that work? Eigenlayer’s mechanism allows existing networks to leverage their trust layer to do other things it was not designed to do. In a concrete example, Eigenlayer provides Ethereum’s trust and economic security to other protocols which want to build on top of it. We highly recommend diving deeper into Eigenlayer. This is very well explained by this Graph presented by the Eigenlayer founder at a16z presentation.

Exhibit 17: In 2015, Ethereum modularised trust and innovation. In 2023, Eigenlayer further modularised the stack by allowing using Ethereum’s trust network to bootstrap and secure Middleware

Even though we continue to see an additional modularisation of the stack (Trust network, Consensus Layer, Execution Layer, Virtual machines, Protocol Apps and dApps), we believe Ethereum remains the key asset and economic powerhouse of the Crypto industry - giving trust, receiving data, enabling permissionless innovation. Although more and more innovation will focus on the Protocol Application and dApp layer, Ethereum’s Trust Network will give credibility to the whole stack. With the help of Eigenlayer, Ethereum has the chance to build the biggest Trust Network in the world while being equally flexible enough to house all other Consensus Protocols on top. Developers can focus on building on top of the trust network, rather than working on the challenging task of bootstrapping one. This means that Ethereum essentially becomes the (Trust)base Layer of the whole Crypto industry.

How Crypto Networks coordinate themselves

In the past paragraphs we looked at Bitcoin’s Trust Network and how Ethereum built a decentralized supercomputer on top of its own trust network. This split innovation and trust, which gave rise to many novel applications. Due to the monolithic nature of Ethereum and its scaling limitations, we have seen an increasing modularisation of blockchains, eventually pushing Ethereum towards a roll-up centric roadmap. Going forward, we believe that Ethereum continues to be at the base center of Crypto and blockchain innovation, seen in the case of Eigenlayer which uses Ethereum’s Trust Network to allow permissionless innovation on the middleware layer. One key question remains - How do cryptonetworks coordinate its decentralized actors?

Exhibit 18: Great explanation from Placeholder VC on how Crypto networks coordinate themselves. For example, in order to start an Ethereum transaction to include the new consensus/data into the public data ledger, you need to pay the stakers (people who include the new blocks of data) some ETH tokens to include them.

5. Comparing the Web3 Stack with Web2 Stack

In the last chapters, we highlighted how Bitcoin and Ethereum rely on open databases, how these databases are kept open and how they are kept operational within a distributed community through token-economic incentives. Relying on different product and technology design choices, this has inevitably led to a different value stack in Web3.

The Web3 stack enables Open Innovation through Composability

Like in Web2, we split the Web3 stack into Protocols and Applications. On the bottom of the Web 3 stack, there is the - extensively discussed - Trust Network relying on thousands of miners and validators. Those reach a consensus on the latest state of the blockchain.